There is a moment in most solar purchases when the financial case shifts from ‘interesting’ to ‘compelling’. For most US homeowners, that moment is when they calculate what the federal solar tax credit actually means in dollar terms for their specific system.

On an average 8kW system costing $24,000 gross, the 30% federal credit is $7,200. On a larger 12kW system for a home with an EV, the credit on a $36,000 system is $10,800. These are not small sums — and they apply to every qualifying homeowner in the US, at every income level, with no lottery or waiting list. You simply install a qualifying system, file Form 5695 with your tax return, and the credit reduces what you owe.

This guide covers everything a homeowner needs to know about the federal solar tax credit in 2026 — its legal basis, how it differs from a deduction, what changed with the Inflation Reduction Act, what the credit covers in full, who qualifies, how the step-down schedule works, and how it interacts with state-level incentives.

The Federal Solar Tax Credit in One Sentence:

| The federal Residential Clean Energy Credit allows US homeowners who purchase and install a solar system to subtract 30% of the total installation cost directly from their federal income tax bill — reducing what they owe the IRS by $5,000 to $10,800 on a typical residential system — and the full 30% rate is available through the end of 2032. |

📊 DOE: U.S. Department of Energy — Homeowner’s Guide to the Federal Tax Credit for Solar Photovoltaics 2026

📌 Also Read:

| → How Much Does Solar Installation Cost? — the full cost breakdown that feeds your credit → Solar Savings Calculator — total 25-year return with tax credit factored in |

What Is the Federal Solar Tax Credit?

The federal solar tax credit — officially called the Residential Clean Energy Credit — is a provision of the US Internal Revenue Code that allows homeowners to claim a tax credit equal to 30% of the cost of a qualifying solar energy system installed at their residence. It is administered by the IRS and claimed on Form 5695 as part of your annual federal income tax return.

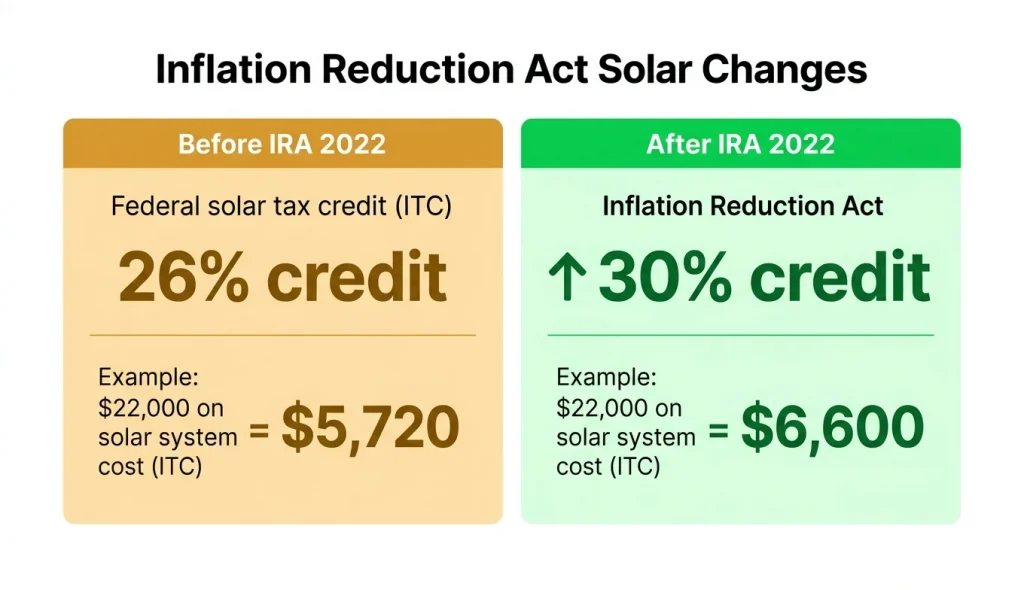

The credit was first introduced in 2006 under the Energy Policy Act, has been extended and modified multiple times since, and was most recently strengthened and extended under the Inflation Reduction Act of 2022. The IRA boosted the credit from 26% (where it stood in 2022) back to 30% and locked it in at that rate through December 31, 2032 — providing a decade of planning certainty for homeowners and the solar industry.

| 30% | $7,200 | No income limit | Rolls forward |

| Credit rate 2022–2032 | Credit on avg $24,000 system | Available to all qualifying homeowners | Unused credit carries to future years |

A Tax Credit vs a Tax Deduction — Why the Distinction Matters

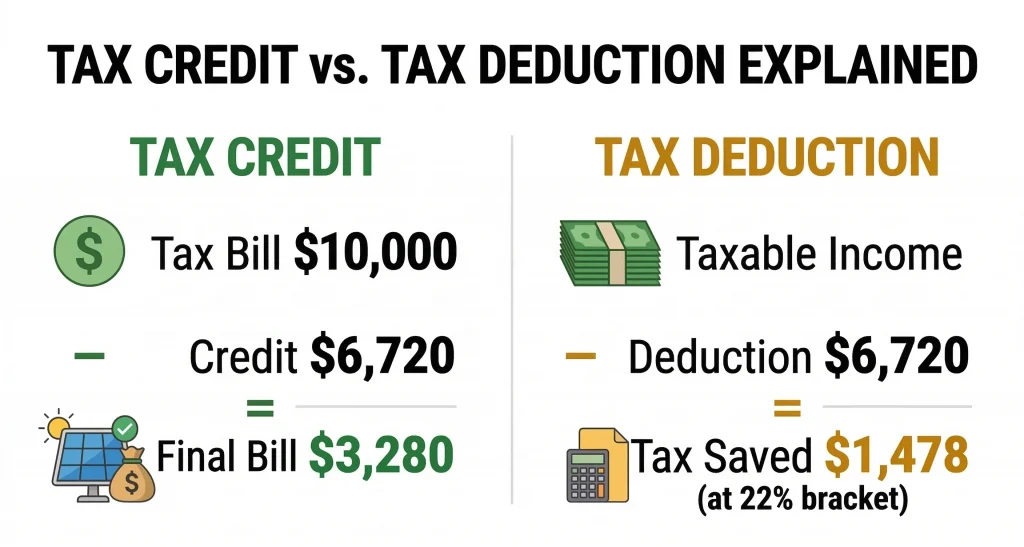

This is the single most important thing to understand about the federal solar ITC. A tax credit and a tax deduction are fundamentally different financial instruments — and the credit is far more valuable.

A tax deduction reduces your taxable income. If you are in the 22% federal income tax bracket and you have a $6,720 deduction, you save $6,720 × 22% = $1,478 in taxes.

A tax credit reduces your tax bill directly, dollar for dollar. A $6,720 tax credit reduces your federal income tax liability by exactly $6,720 — regardless of your tax bracket.

In our example, the credit saves you $5,242 more than the deduction would. That is not a rounding difference — it is a difference that determines whether the system pays back in 7 years or 10 years.

📊 IRS: IRS — Residential Clean Energy Credit Official Publication 2026

What the Inflation Reduction Act Changed for Solar Homeowners

The Inflation Reduction Act of 2022 (IRA) made four significant changes to the residential solar tax credit that homeowners need to understand:

1. The Credit Rate Was Restored to 30%

Before the IRA, the residential solar credit had been stepping down. In 2022 it was at 26% before the IRA was signed. The IRA retroactively restored it to 30% for systems installed from 2022 onward and locked it there through 2032. Any homeowner who installed in early 2022 before the IRA was signed and claimed 26% may have been able to file an amended return to claim the additional 4%.

2. Battery Storage Now Qualifies as a Standalone Credit

Before the IRA, battery storage only qualified for the solar ITC if installed simultaneously with a new solar system. The IRA expanded this to allow standalone battery storage — a battery installed separately, without being paired with a solar installation in the same project — to qualify for the full 30% credit. The only requirement is that the battery has a capacity of at least 3 kWh, which covers all residential home battery systems currently on the market.

This means a homeowner who installed solar in 2020 and now wants to add a battery can claim 30% of the battery cost independently — a credit of $3,000 to $4,500 on a typical Powerwall or similar installation.

3. The Step-Down Schedule Was Revised

The previous credit schedule had complex step-downs that were difficult to plan around. The IRA simplified this: 30% through 2032, then 26% in 2033, 22% in 2034, and 0% for residential installations from 2035 onward (commercial retains 10%). This clear long-term schedule means homeowners can plan their installations with certainty about their credit amount.

4. Expanded Coverage for Additional Technologies

The IRA also expanded the Residential Clean Energy Credit to cover geothermal heat pumps and small wind energy systems at the 30% rate — alongside solar PV and solar thermal systems that were already covered. This guide focuses on solar, but the same credit mechanics apply to these other qualifying technologies.

📊 Congress.gov: Inflation Reduction Act of 2022 — Clean Energy Tax Credit Provisions Full Text

Who Qualifies for the Federal Solar Tax Credit in 2026?

The federal solar ITC has no income limits and no geographic restrictions — it is available to any US homeowner who meets the following conditions:

| Condition | Requirement | Common Pitfall |

| System ownership | You must own the system outright (cash or loan) | Lease / PPA = company owns system, company claims credit |

| Property use | Primary or secondary personal residence | Pure rental investment property does not qualify |

| New installation | System newly installed in the credit year | Existing systems already in service do not generate a new credit |

| Operational status | System must be installed and generating power before Dec 31 of the credit year | Installation in December — confirm commissioning date |

| Federal tax liability | Must have federal income taxes owed to apply the credit against | Credit rolls forward — low earners can still claim over time |

| System standards | System must meet applicable fire and electrical codes | Hire NABCEP-certified installers who ensure compliance |

The absence of an income limit is genuinely significant. Unlike many means-tested government programmes, the solar ITC is available at full value to both a homeowner earning $45,000 per year and one earning $450,000 per year — provided both have sufficient federal income tax liability to use the credit.

What the Federal Solar ITC Covers — Complete Breakdown

The credit applies to the full installed cost of a qualifying solar energy system. Here is exactly what is included and excluded:

| Cost Item | Qualifies? | Notes |

| Solar PV panels (all types) | ✅ Yes | Monocrystalline, polycrystalline, thin film |

| String inverters | ✅ Yes | All inverter types qualify |

| Microinverters and power optimisers | ✅ Yes | Full cost qualifies |

| Mounting hardware and racking | ✅ Yes | Roof and ground mount both qualify |

| All labour and installation costs | ✅ Yes | Including subcontractors |

| Electrical wiring, conduit, junction boxes | ✅ Yes | All system wiring qualifies |

| Permit and inspection fees | ✅ Yes | Fees paid as part of the project |

| Battery storage (with or without solar, 3kWh+) | ✅ Yes | Standalone battery now qualifies post-IRA |

| Solar monitoring systems | ✅ Yes | Included in full system cost |

| Roof repairs required specifically for solar mount | ✅ Partial | Only the portion directly needed for solar installation |

| New roof replacement | ❌ No | Roof work not required by solar does not qualify |

| Extended service and maintenance contracts | ❌ No | Post-installation services do not qualify |

| Solar leases and PPAs | ❌ No | You must own the system to claim the credit |

| Off-grid generator systems (fuel-based) | ❌ No | Must be solar / renewable technology |

📌 Also Read:

Federal Solar Tax Credit Amounts — What You Actually Get

Here is the real-dollar impact of the 30% federal ITC across the full range of residential system sizes in 2026. All gross costs use 2026 US average pricing of $2.80 to $3.10 per watt installed:

| System Size | Gross Cost | 30% ITC Credit | Net Cost | Monthly Saving (avg US) | Payback Period |

| 4 kW | $11,200–$12,400 | $3,360–$3,720 | $7,840–$8,680 | $80–$110/mo | 13–16 yrs |

| 5 kW | $14,000–$15,500 | $4,200–$4,650 | $9,800–$10,850 | $100–$140/mo | 10–13 yrs |

| 6 kW | $16,800–$18,600 | $5,040–$5,580 | $11,760–$13,020 | $120–$165/mo | 9–11 yrs |

| 7 kW | $19,600–$21,700 | $5,880–$6,510 | $13,720–$15,190 | $140–$190/mo | 8–10 yrs |

| 8 kW | $22,400–$24,800 | $6,720–$7,440 | $15,680–$17,360 | $160–$220/mo | 7–9 yrs |

| 10 kW | $28,000–$31,000 | $8,400–$9,300 | $19,600–$21,700 | $200–$275/mo | 7–9 yrs |

| 12 kW | $33,600–$37,200 | $10,080–$11,160 | $23,520–$26,040 | $240–$330/mo | 7–8 yrs |

| 8kW + 10kWh battery | $34,400–$38,800 | $10,320–$11,640 | $24,080–$27,160 | $160–$220/mo | 9–11 yrs |

The battery-inclusive row illustrates how the IRA’s expanded battery credit compounds the benefit. A homeowner installing an 8kW solar system with a 10kWh home battery can claim a combined credit of $10,320 to $11,640 — reducing a $38,000 gross investment to under $27,000 net in a single tax year.

How the Federal ITC Interacts with State Solar Incentives

The federal ITC does not limit your ability to claim state-level incentives — the two typically stack independently. However, there are some important interactions to understand:

State Tax Credits Stack Directly

States with their own solar tax credits (Hawaii at 35%, South Carolina at 25%, Maryland at 30%, Montana at 100% up to caps) allow homeowners to claim both the federal and state credit independently. On a $22,400 system in Hawaii, the federal 30% credit ($6,720) and state 35% credit (capped at $5,000) can together reduce your net cost to $10,680 — less than half the gross installation cost.

State Rebates May Affect Your Federal Credit Basis

Cash rebates received directly from a state government or utility company can reduce your federal credit calculation basis in some circumstances. Specifically, rebates paid to you directly (as opposed to paid to your installer) may reduce the ‘amount paid’ for the system from the IRS’s perspective. This is a nuanced area — consult a tax professional if you receive a significant state cash rebate alongside your federal credit, particularly for systems with business or rental components.

Property Tax Exemptions and Sales Tax Exemptions Are Separate

Most states that offer solar property tax exemptions (exempting the added home value from solar from property tax assessment) and sales tax exemptions (no sales tax on solar hardware) apply these automatically — they are not claimed on any tax return and do not interact with the federal ITC. These are effectively free additional savings that layer on top of the credit without any coordination required.

| State | Top State Incentive | Value | Stacks with Federal? | Combined Net Cost (8kW) |

| Hawaii | State ITC 35% (cap $5,000) | Up to $5,000 | ✅ Yes | ~$8,600 net |

| New York | NY-Sun + state credits | $7,000–$9,000 | ✅ Yes | ~$8,000–$10,000 net |

| Massachusetts | SMART programme income | $100–$400/yr×10 | ✅ Yes | $17,000 net + income |

| New Jersey | SREC quarterly income | $150–$400/yr | ✅ Yes | $16,000 net + income |

| Illinois | Illinois Shines SRECs | $2,000–$6,000 | ✅ Yes | $10,000–$14,000 net |

| South Carolina | State ITC 25% (cap $3,500) | Up to $3,500 | ✅ Yes | ~$12,000 net |

| Maryland | State credit 30% (cap $1,000) | Up to $1,000 | ✅ Yes | ~$14,600 net |

The Federal ITC Step-Down Schedule — Act Before 2033

While the 30% rate runs through 2032, it is worth understanding the step-down schedule that begins in 2033 — because the financial impact of waiting is substantial:

| Year | Credit Rate | Credit on $24,000 System | vs 2026 Credit | Difference |

| 2026 (now) | 30% | $7,200 | Baseline | — |

| 2033 | 26% | $6,240 | −$960 | ⚠️ Lose $960 |

| 2034 | 22% | $5,280 | −$1,920 | ⚠️ Lose $1,920 |

| 2035+ | 0% | $0 | −$7,200 | ❌ No credit |

The message is clear: there is no financial benefit to waiting beyond 2032 for a planned solar installation. Homeowners who delay from 2026 to 2033 lose $960 in credit on a $24,000 system. Those who delay to 2034 lose $1,920. Those who miss the residential window entirely by waiting to 2035 lose the full $7,200. Any homeowner seriously considering solar in the next few years benefits from acting before 2033.

Federal Solar Tax Credit: 10 Most Common Questions Answered

Does the federal solar tax credit expire in 2026?

No — the federal solar tax credit is available at the 30% rate through December 31, 2032, following the Inflation Reduction Act of 2022. The credit is not expiring in 2026. It begins to step down in 2033 (26%), reduces further in 2034 (22%), and expires for residential installations in 2035. Homeowners installing solar any time through 2032 receive the full 30% credit.

Can I claim the credit if I finance solar with a loan?

Yes — the federal solar ITC applies equally whether you purchase your system with cash or finance it with a solar loan. What matters is ownership of the system — if you take out a loan to buy the system, you own it from day one and qualify for the full credit. Solar leases and PPAs do not qualify because the leasing company, not you, owns the system.

What if my tax liability is less than my credit?

If your federal income tax liability for the installation year is less than your solar credit, the unused portion carries forward to subsequent tax years. For example, if your credit is $7,200 but you only owe $4,500 in federal taxes, you claim $4,500 this year and carry the remaining $2,700 forward to next year’s return. The carryforward continues until the full credit is used, with no time limit within the credit’s eligibility window (through 2032 at 30%).

Can renters claim the federal solar tax credit?

No — the federal solar ITC is available only to homeowners who install solar on a property they own. Renters cannot claim the credit for a landlord’s solar installation, and landlords installing solar on a pure rental property claim the commercial ITC (also 30%) rather than the residential credit. Community solar programme credits provide an alternative for renters to access some solar financial benefits in states where community solar programmes exist.